Understanding how to shop for a mortgage takes some leg work, but it’s proven to be worth it.

Research from Freddie Mac showed borrowers who got multiple rate quotes saved between $600 and $1,200 annually on their home loan. And negotiating your rate may drive even greater savings.

When shopping for a mortgage, you have to get quotes from three or more lenders. This involves giving each lender basic information about your finances and the home you want to buy, and then comparing their offers.

All told, you could save thousands by comparing rates — even tens of thousands. Here’s what to do.

In this article (Skip to…)

Shopping for a mortgage is almost guaranteed to save you money because all mortgage companies offer different rates to different borrowers. And if you know what you’re doing, it doesn’t have to be difficult or time-consuming.

Learning how to shop for a mortgage isn’t all that hard. At least, not if you know what to expect. Here’s how the process will go:

Mortgage companies use credit scores to decide who gets approved for a home loan and what mortgage interest rates they’ll pay. Typically, the higher your credit score, the lower your rates will be.

Annualcreditreports.com provides free copies of your credit reports from the three major credit bureaus: TransUnion, Equifax, and Experian. If your scores are low, then spend some time in the early months of your home-buying journey to improve your scores. Good credit scores will not only help you get approved for a mortgage loan, but they can also save you thousands of dollars over the life of your loan.

Paying down high-interest credit card debt, student loans, and personal loans will increase your score. As will ensuring timely payments for current utility bills, rent, and installment loan repayments. Review our guide to improving low credit scores for more information.

Home buyers have a selection of home loans from which to choose. Having a general understanding of the benefits and requirements for each of these different types of mortgage loans will help you find the most advantageous path to homeownership.

Conventional loans are a popular type of loan, accessible with a minimum FICO score of 620 and a down payment as low as 3%. Additionally, lenders evaluate your debt-to-income ratio, credit history, and employment stability, usually preferring a debt-to-income ratio under 43%.

If you’re able to make a down payment of 20% or more, you’ll be exempt from the mandatory private mortgage insurance (PMI) payments. Additionally, once your loan-to-value ratio reaches 78%, lenders usually remove the PMI. Furthermore, refinancing options are available to eliminate PMI from your loan once you’ve built up at least 20% equity in your home.

You can choose from various loan lengths, typically between 10 to 30 years, and opt for either a fixed or adjustable interest rate. Fixed rates provide consistent monthly payments, while adjustable rates might start lower but can fluctuate over time.

FHA loans are backed by the Federal Housing Administration (FHA). This type of loan is a favorite among first-time home buyers due to their lenient qualification criteria. You can secure an FHA loan with just 3.5% down if your FICO score is 580 or above, or with a 10% down payment for scores as low as 500.

However, it’s important to note that FHA loans mandate mortgage insurance premiums (MIP) for the entirety of the loan’s term. Nonetheless, there’s an option to eliminate this MIP in the future by refinancing into a conventional loan.

FHA loans also have specific guidelines for the debt-to-income ratio and property standards. The property being purchased must meet certain safety and security standards and undergo an FHA appraisal. This is to ensure the home’s value justifies the loan amount and it meets minimum property standards.

VA loans, backed by the Department of Veterans Affairs, provide a significant benefit of 0% down payment but are exclusively available to eligible veterans or service members. Although the VA itself doesn’t specify a minimum credit score, individual lenders often impose their own requirements, usually ranging between 580 to 620.

In addition to the no down payment feature, VA loans do not require mortgage insurance, resulting in lower monthly payments. However, there is a VA funding fee, which is typically between 1.3% to 3.6% of the loan amount. It’s important to note that while the VA provides guidelines, individual lenders may have additional criteria for income stability and debt-to-income ratios.

The U.S. Department of Agriculture (USDA) loan is specifically designed for low-income buyers in certain suburban and rural areas. This loan stands out because it requires no down payment. While the USDA does not establish a minimum credit score requirement, most lenders prefer to see a FICO score of around 640.

USDA loans aim to support homebuyers who might not qualify for conventional mortgages due to financial constraints. They offer several advantages, such as lower interest rates and reduced mortgage insurance costs compared to conventional loans. However, applicants must meet certain income eligibility criteria, which vary based on the region and household size.

Additionally, the property must be located in an eligible rural or suburban area as defined by the USDA. These loans also typically require the property to be the buyer’s primary residence and to meet specific safety and quality standards.

Jumbo loans are a type of mortgage that exceeds the conforming loan limits set by the Federal Housing Finance Agency (FHFA). This makes them ideal for financing high-priced or luxury properties that go beyond the scope of conventional mortgages.

Unlike conventional loans, jumbo loans cannot be secured by government-sponsored entities like Fannie Mae or Freddie Mac. As a result, they often have more stringent credit requirements. Typically, lenders look for higher credit scores, usually around 700 or above, for jumbo loan applicants. Additionally, these loans often require larger down payments, commonly 20% or more of the home’s purchase price, to offset the lender’s increased risk.

Lenders primarily offer two types of mortgages: adjustable and fixed-rate loans. And the type of loan you choose, will directly impact the rate you’ll be given.

Fixed-rate loans have a set interest rate that doesn’t change during the loan’s term. Common loan terms are 15-year and 30-year mortgages, which means you’ll make monthly mortgage payments for 180 months and 360 months, respectively.

Adjustable-rate loans have variable interest rates that change over the life of the loan. Your initial rate is often fixed for a period of time, but will reset periodically over your 15- or 30-year loan term

When you’re looking to finance a real estate purchase or new home, mortgage companies will need proof of your income, assets, and credit to give you an accurate rate quote. So start compiling the paperwork you’ll need on your application, like bank statements and recent pay stubs, early on in the mortgage shopping process.

Most experts recommend getting at least three rate quotes when you shop for a mortgage. But there’s no limit to the number of mortgage companies you can apply with. And research suggests that the more quotes you get, the more money you’ll save.

For example, Freddie Mac found that “borrowers who received as many as five rate quotes during the second half of 2022 could have potentially saved more than $6,000 over the life of the loan, assuming the loan remains active for at least five years.”

You should get at least 3-5 mortgage quotes when shopping for a home loan. The more quotes you get, the more you’re likely to save.

When learning how to shop for a mortgage loan, it’s essential to compare offers from multiple sources to ensure you land the best deal and the lowest rate.

Each of these sources can provide different benefits, from lower rates to more flexible terms, especially if you’re considering a refinance. It’s important to compare their offers carefully to find the one that best fits your financial situation.

“Keep in mind that a quote is just that, and nothing is guaranteed until you are locked in,” reminds Jon Meyer, mortgage loan expert and licensed MLO. “But quotes should help you gauge the market, lender to lender.”

Mortgage rates are higher than the rates we saw several years ago — around % ( % APR) for 30-year fixed-rate loans. Interest rates and annual percentage rates are for sample purposes only. See our full loan rate assumptions here.

For perspective, the long-time average for 30-year fixed mortgage rates is about 8%. That’s the average since Freddie Mac’s records began in 1971.

But keep in mind that not everyone gets the same rates.

The best mortgage rates are reserved for “top-tier” borrowers. Those are people with:

Of course, few borrowers are “perfect.” Most of us fall somewhere on the spectrum between excellent and so/so personal finances.

Where you are on that spectrum will determine the mortgage rates you qualify for. But knowing how to shop for a mortgage will help you make sure your deal is at the better end of that range.

Experiment with a mortgage calculator to see how down payment, rate, and loan term affect your monthly mortgage payment and how much home you can afford.

At face value, comparing mortgage rates is fairly straightforward.

You can apply for preapproval with three or more lenders and simply compare the rates you’re offered. But remember — your interest rate isn’t the only thing that matters. You also need to look at factors like closing costs, origination fees, annual percentage rate (APR), and discount points.

Luckily, it’s easy to compare mortgage quotes and find the best deal.

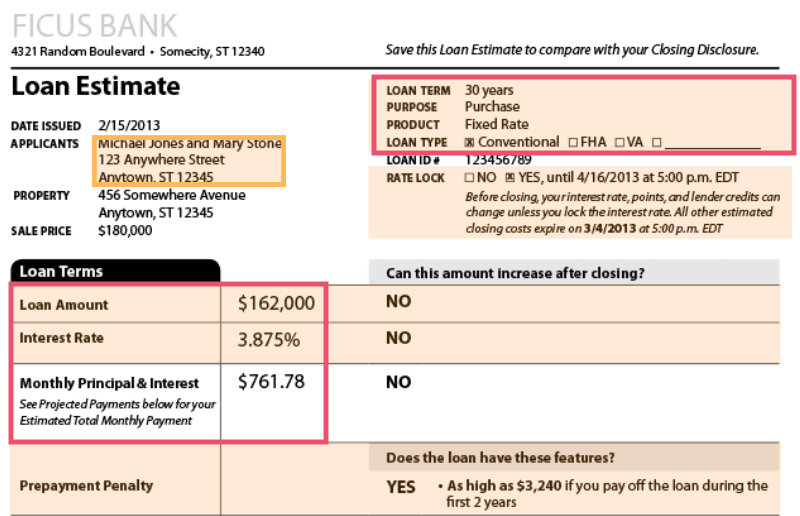

You will find your loan terms, quoted interest rate, and monthly payment on the first page of your Loan Estimate.

Along with comparing interest rates, you can use this page to:

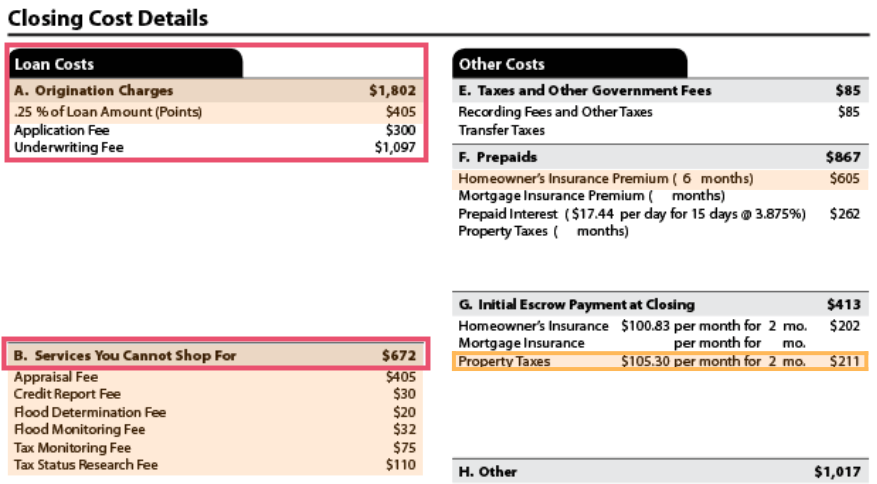

On the second page, you will see your closing costs and other upfront expenses, like prepaid taxes and homeowners insurance.

Note that loan costs are separated into two categories: (A) Origination Charges, and (B) Services You Cannot Shop For.

Origination charges represent the lender’s own fees. You’ll want to pay close attention to this section when shopping for a mortgage because these fees can vary a lot from one lender to the next. Shopping for a lower fee could save you serious cash at the closing table.

In addition, this section includes information on “Points.” Points — or discount points — are an additional fee paid upfront to get a lower interest rate.

You’ll want to pay attention to discount points when shopping for mortgage rates. If one mortgage lender has exceptionally low rates, but charges points, you know you have to pay extra upfront to actually get that rate.

Because these documents are uniform, it’s easy to compare Loan Estimates from different lenders side by side and find the very best deal on your rate and closing costs.

Keep in mind that the mortgage quotes you get are not set in stone. Mortgage lenders have the flexibility to adjust their fees and even their interest rates. That means you can often use competing offers as leverage to negotiate your costs.

Don’t hesitate to play one lender off against another:

“I like your company, but I’ve got a quote here with a lower rate or less expensive closing costs. Can you match it? Better yet, can you beat it?”

Chances are, these negotiations won’t lower your rate by much. But, when you’re borrowing huge amounts over decades, even a tiny drop in your rate can add up to hundreds or even thousands. And what do you have to lose?

Once you’ve put in your applications, compared interest rates and fees, and chosen your preferred lender, there are a few final steps to take in order to finalize your mortgage loan.

Once you’ve found your dream home and successfully negotiated the purchase price with the seller, it’s time to begin the formal mortgage application process.

Although you may have already been preapproved for a mortgage, you’ll need to go through a similar, but more rigorous, underwriting process in order to receive final approval.

The underwriter will verify all your financial information and documentation. It may request additional verifications or a letter of explanation, so stay on top of the process and respond to any queries as soon as possible. This will help keep your loan process and closing date on track.

Try to avoid changing jobs or becoming unemployed, if at all possible. And don’t open or close any credit accounts. Any of the last three could reduce your credit score. “Also, don’t make any large purchases on open credit lines,” adds Meyer.

Keep in mind that lenders routinely recheck your credit history just before closing. So you don’t want to do anything that will jeopardize your savings, mortgage rate, or — worst case — your entire mortgage approval.

Aim to get at least three mortgage quotes. This will give you a good idea of the range of mortgage rates you qualify for. Ideally, get five or more quotes in order to find the very best rate and maximize your savings.

What do you need to know when you shop for a mortgage?The biggest thing you should know is that lenders cannot tell you your mortgage rate until you’ve been preapproved for a mortgage loan. So in order to shop for a mortgage, you need to actually apply — and provide documents — with more than one lender. This takes some time, but it’s the only “real” way to find your best deal. Looking at advertised rates online won’t help you.

What’s the difference between prequalified and preapproved?Getting prequalified can be a helpful first step in the home buying process. Prequalification involves answering a few questions about your financial situation, after which a loan officer will tell you whether you might be mortgage-qualified and what your maximum loan amount is likely to be. Mortgage preapproval, on the other hand, is a more rigorous process that involves supplying financial documents and going through a credit check and underwriting. After this, you’ll have a verified approval and know your final loan amount and interest rate. Preapproval is often required to make an offer on a house.

Can I have two mortgage offers?Yes. You can have as many mortgage offers as you want. You are never obligated to work with a mortgage lender until you’ve signed final closing documents, so there’s no danger in applying with more than one company. The only thing to look out for is whether lenders have application fees. Ideally, you want to shop around with lenders that won’t charge you a fee to apply and check your rate.

How should I choose a mortgage lender?You can narrow down your initial list of lenders based on recommendations, online reviews, advertised rates, and availability of the loan product you need. Once you’ve chosen 3-5 mortgage companies that look promising, you can apply for preapproval with each one. Then compare the Loan Estimates they give you to find the best combination of interest rates and upfront fees for your situation.

Does shopping for a mortgage hurt your credit?Lenders do a hard credit pull when you apply for preapproval, which typically hurts your FICO score by five points or less. But as long as you get all your mortgage quotes within 2-4 weeks of each other, any hard inquiries during that time will count as a single inquiry. So your score will not be dinged multiple times. Aim to get all your quotes on the same day, if possible, as this will give you the most accurate comparison between lenders.

How long does it take to get approved for a mortgage?From application to closing, the mortgage process typically takes around 30-45 days. This can vary depending on how complicated your loan application is, how fast you respond to your lender’s requests, and outside factors like how busy the lender is or how long it takes to get a home appraisal done.

How do I get the best mortgage rate?Your mortgage rate is largely based on your personal finances. To get the best rate possible, start improving your credit and paying down debts six months to a year before you want to buy a house. Try to keep credit card balances below 30 percent of their limit. You can also lower your mortgage rate by making a bigger down payment. Finally, be sure to compare rates from at least 3-5 lenders. Interest rates vary a lot by company, so shopping around can help you find the best deal.

Curious about securing the best mortgage deal in today’s market?

The key is in knowing how to shop for a mortgage effectively. Start by gathering multiple quotes and then diligently compare them.

Ensure that each loan offer has similar terms and identical rate lock periods. This comparison process is straightforward and can conveniently be done online.

Want to explore your current home buying options further? Click through to find out more about how to shop for a mortgage and unlock the best deals available now.

Authored By: Peter Warden The Mortgage Reports EditorPeter Warden has been writing for a decade about mortgages, personal finance, credit cards, and insurance. His work has appeared across a wide range of media. He lives in a small town with his partner of 25 years.

Updated By: Ryan Tronier The Mortgage Reports EditorRyan Tronier is a personal finance writer and editor. His work has been published on NBC, ABC, USATODAY, Yahoo Finance, MSN Money, and more. Ryan is the former managing editor of the finance website Sapling, as well as the former personal finance editor at Slickdeals.

Reviewed By: Paul Centopani The Mortgage Reports EditorPaul Centopani is a writer and editor who started covering the lending and housing markets in 2018. Previous to joining The Mortgage Reports, he was a reporter for National Mortgage News. Paul grew up in Connecticut, graduated from Binghamton University and now lives in Chicago after a decade in New York and the D.C. area.